What exactly is a journal?

A journal is where a company records all of its transactions in chronological order. When you record these transactions it is called journalizing. An example would be if a company bought office equipment they would need to record this in one of their journals. Every journal entry has a debit and a credit and the two must equal.

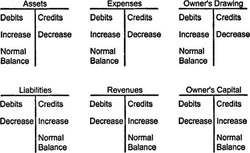

Debits & Credits

table 1

What is a debit?

A debit is recorded on the left side of the T account. (see table 1.) When the left side is increased this is known as the normal balance. When an asset is on the left side it has a normal debit balance.

What is a credit?

A credit is shown on the right side of a T account. Any liability that is increased on the right side has a normal credit balance.

A debit is recorded on the left side of the T account. (see table 1.) When the left side is increased this is known as the normal balance. When an asset is on the left side it has a normal debit balance.

What is a credit?

A credit is shown on the right side of a T account. Any liability that is increased on the right side has a normal credit balance.

Special Journals

A special journal is only used to record one kind of transaction. Some examples of a special journal would be purchases, cash payments, sales, and cash recipets. The general journal is used to record any other transaction. In a purchases journal the company will record all merchandise that they buy on account. For cash payments the company records anything that they pay cash for. (pretty obvious by the account name.) In the sales journal all of the company's sales are recorded that are made on account. And finally in the cash receipts journal, this is where all the receipts are recorded.